Risk-adjusted property-catastrophe rates-on-line in Japan reverted back to levels last seen in the early 2020s at the April 1 2026 reinsurance renewals, with catastrophe excess-of-loss programmes in the country witnessing risk-adjusted price reductions of up to 20%, according to Howden Re, the global reinsurance broker.

At the Japan-focused April renewal season, Howden Re notes a continuation of the softening trend seen at January 1, in spite of the uncertain and volatile geopolitical landscape in the Middle East, which the broker says drove acute stress across multiple specialty lines around the world.

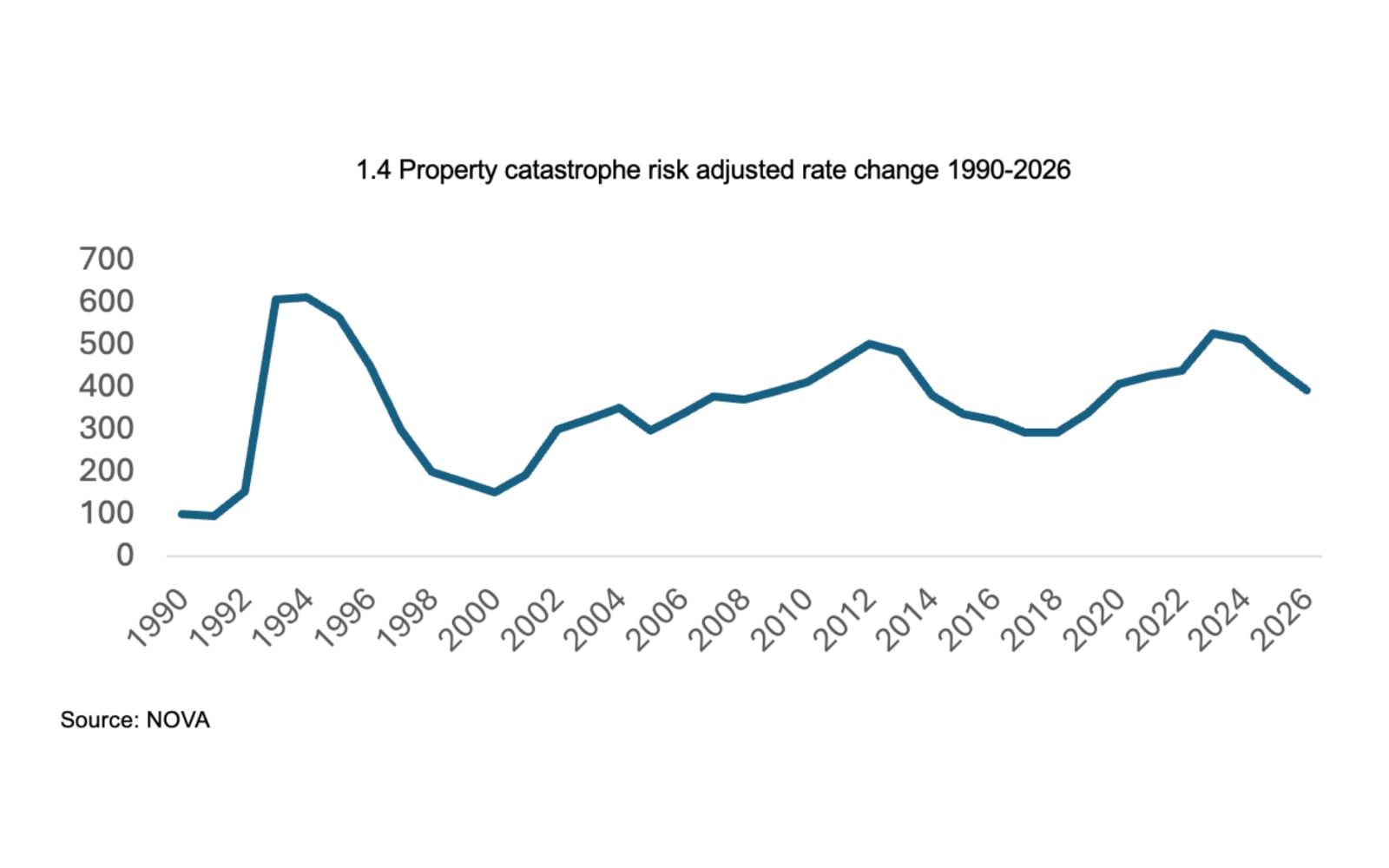

Risk-adjusted price reductions on Japanese catastrophe excess-of-loss programmes of as much as 20%, with a point estimate of 16%, occurred on the back of benign global property cat market conditions, and another year of low catastrophe losses in Japan.

Howden Re states that within proportional reinsurance business, commissions on property surplus and earthquake quota share treaties rose between 2% and 5% at 1.4, with the upper end of the range most commonly achieved on quake quota share agreements.

Andy Souter, Head of Asia Pacific, Howden Re, said: “Japan rates are now broadly back to early twenties levels. Strong reinsurer appetite, improving underlying performance, and a lack of major loss activity have all contributed to cedent-friendly outcomes at this renewal.”

The image below, provided by Howden Re, shows the April 1 property cat rate change between 1990 and 2026.

Importantly, Howden Re emphasises a continuation of discipline among reinsurers during the renewal period, although some sellers did look for opportunities to grow their shares.

“Overall, the balance of supply and demand remained broadly consistent with the previous year; programme structures were largely unchanged from expiring terms, with only limited instances of additional purchases or structural adjustments,” explains Howden Re.

Outside of Japan, Howden Re says that the 1.4 renewals support the notion reinsurer balance sheets remain strong and that appetite for well-structured risk transfer programmes also remains robust.

“The orderly completion of the renewal, with no structural disruption, disciplined capacity and cedent-friendly pricing outcomes, is testament to the underlying health of the market even in a period of heightened geopolitical uncertainty,” explains the broker.

While the Strait of Hormuz remains effectively closed following the US and Israel conflict with Iran, this had no direct impact on property cat renewals at 1.4, with any dislocation mainly focused in the specialty market, according to the broker.

“This renewal was completed in a largely benign property-catastrophe environment, insulated from the immediate disruption in the Gulf,” said David Flandro, Head of Industry Analysis and Strategic Advisory at Howden Re. “That said, a sustained energy supply shock raises the risk of renewed inflationary pressure and higher interest rates, dynamics that have historically affected reinsurance capital and pricing across all lines, not just those directly exposed to the conflict.”

In terms of the mid-year 2026 reinsurance renewals, Howden Re expects buyers and sellers to face more complex conditions globally, with upward pricing pressure expected across marine, energy, and political violence as the full impact of the Hormuz situation is absorbed. Howden Re expects this to result in reinsurers reassessing aggregation, event definition, and Middle East exposure in their specialty portfolios.

“The reinsurance market remains well capitalised and engaged. Technical discipline, transparency and active monitoring are essential as we move into what is shaping up to be a more complex mid-year environment,” added Souter.