Underwriting income from reinsurance business over the last decade has been far more significant for Bermudian re/insurers than underwriting income from primary business, but this hasn’t stopped firms’ continued transition to a more insurance focused business mix, according to Fitch Ratings.

Global financial services rating agency, Fitch Ratings, has examined the performance of a group of 15 Bermudian re/insurers from 2007 – 2016, of which four are no longer independent, and found some interesting, yet concerning results.

The report, Bermuda Market Long-Run Performance, highlights the steady decline of the group of re/insurers operating return on equities (ROEs) over the ten-year period, from a high of 20.3% in 2007 to 7.4% in 2016.

Unsurprisingly, as the soft market has persisted and been exacerbated by the inflow of alternative reinsurance capital and the benign loss environment, Fitch underlines the deterioration of the group of re/insurers’ combined and operating ratios during the period.

In the softening cycle reinsurance business has seen its profitability decline and as a result companies have looked to primary business for less competition and greater returns, both in the Bermuda market and around the world.

Fitch explains that this has been the case with the group of 15 Bermuda-based re/insurers, as reinsurance market conditions remain more challenging than insurance. According to Fitch, from 2007 – 2016 reinsurance segment gross premiums written (GPW) for the group declined to 44% of the 2016 aggregate GPW from 53% of the 2007 total, while the insurance segment increased from 43% in 2007 to 51% in 2016.

Over the ten-year period the group of Bermudian re/insurers experienced an overall GPW CAGR (compound annual growth rate) of 4%, with the insurance segment producing the highest growth at 6%, and reinsurance business increasing by just 2%.

The chart below, provided by Fitch, shows that over the last two years insurance business has dominated GPW for the group, which was not the case in each year from 2007 – 2013, when reinsurance business dominated.

The increased focus on primary business is a reaction to the more challenging conditions seen in the reinsurance sector, and Fitch expects the trend to continue, albeit less dramatically, as reinsurance pressures persist but the primary market becomes more competitive, too.

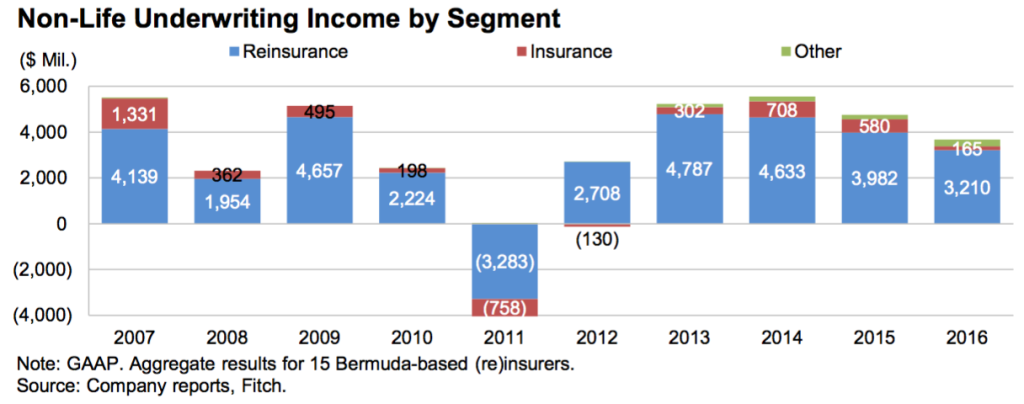

But despite the transition to what appears to be the more profitable, or at least less competitive primary insurance business over the reinsurance marketplace, the latter continues to drive much of the underwriting income for the group.

“Companies shifted business from reinsurance to insurance as reinsurance margins declined, but they have yet to produce consistent favorable insurance underwriting results. The group produced a 90.5% total calendar year (CY) combined ratio with a very strong 84.5% in reinsurance offset by a much higher 97.5% in insurance.

“Future Bermuda market results could suffer from a business mix shift to insurance and continued reinsurance segment earnings pressure, although volatility could be reduced,” explains Fitch.

According to Fitch, over the ten-year period the group of re/insurers were “heavily reliant on underwriting income sourced from reinsurance business,” with 87% of non-life underwriting income coming from reinsurance operations, compared with just 10% from insurance and 3% from other sources.

Furthermore, the proportion of underwriting income from each segment is in contrast to the GPW sector split of 49% in reinsurance, 47% insurance, and 3% life and health, and 1% other, explains Fitch.

“The fact that reinsurance underwriting income has been a much more significant contributor to total non-life underwriting income than insurance is very concerning as companies continue to shift business away from reinsurance.

“Future underwriting profitability will be squeezed from both a shift in business mix to less profitable insurance business and as a result of declining margins in reinsurance business. Favorably, as the proportion of reinsurance business declines, the risk profile of Bermuda companies should improve with less volatile overall results,” says Fitch.

The above chart, provided by Fitch, shows that reinsurance underwriting income has been a far more significant contributor to the groups’ performance than insurance, over the ten-year period.

Overall, Fitch expects the recent trend of Bermudian re/insurers turning their focus to primary business to persist as the softening reinsurance cycle continues to hinder operations on this segment. However, so far, insurance business is failing to generate the kind of returns some in the sector might have been hoping for, and reinsurance underwriting income remains highly significant for the group.

It will be interesting to see how re/insurers in both Bermuda and around the world continue to balance their reinsurance and insurance business segments, as competition in the primary sector looks set to increase as reinsurance market headwinds persist, and possibly intensify.