The impacts of the COVID-19 pandemic on the global economy is expected to mitigate organic growth for insurance brokers, but firms cost saving initiatives and a hardening commercial lines market could offset some of the negative pressures, according to analysts at Wells Fargo Securities.

It’s going to be some time before the financial impact of the COVID-19 pandemic is well understood, while for industries and businesses of all shapes and sizes uncertainty remains against a backdrop of widespread remote working social distancing efforts.

It’s going to be some time before the financial impact of the COVID-19 pandemic is well understood, while for industries and businesses of all shapes and sizes uncertainty remains against a backdrop of widespread remote working social distancing efforts.

Examining the performance of insurance brokers in light of the challenging and volatile financial market landscape, analysts at Wells Fargo Securities note that first-quarter results should still benefit from strong GDP growth. However, the economy is expected to continue weakening and with negative GDP growth on the horizon, analysts have cut their EPS estimates for Q2 2020.

“On average our 2020 and 2021 EPS estimates drop by just over 3% in both years, which compares to the 25.5% drop we have seen in the price of the sector since the middle of February. The sector is now trading at around 14.5x our 2021 cash EPS estimates, which seems attractive to us, given the pullback we have seen so far this year,” explains Wells Fargo Securities in a recent report.

Despite lowering its price targets to reflect the potential for a negative quarter or two, analysts add that brokers are still viewed as offering a good place for investors to play the insurance sector. Exactly what shape the resulting economic cycle from the pandemic will be remains unclear, but if V-shaped, analysts note that the quick recovery is supportive of strong organic prospects at year-end 2020 and heading into 2021.

“Further, brokers have no pulls on their capital so whereas underwriters could feel a capital crunch if claims costs rise and they sit hits to their investment portfolios that is not the case for insurance brokers,” continues to report.

The last time the global economy experienced this level of uncertainty and stress was during the 2008 financial crisis. And, while this can be a proxy of the slowdown that could be seen in Q2 for brokers, analysts at Wells Fargo Securities warn that it’s not quite so straightforward.

While negative GDP growth was a feature of the market in 2008 as is the case now, insurance brokers also had to deal with a soft insurance market and an economic slowdown that was more pronounced in the U.S. when compared with the rest of the world. Of course, the economic slowdown in the U.S. is expected to be significant, but that’s also the case for many other countries in all parts of the world.

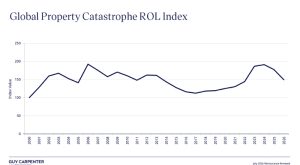

Furthermore, and as highlighted by analysts, brokers have the backdrop of a hardening commercial lines market that is expected to get harder as low interest rates persist. According to analysts, additional hardening can help to offset some of the pressures from the fading economy and negative GDP growth.

Of course, the fact that companies have gone remote and the large majority of travel has stopped, there could be a slowdown of new business in the broker space. Although, Wells Fargo Securities says that in contrast, the market could also see some higher-then-normal levels of retentions at some of the larger brokerage firms.

Additionally, cost saving programs, such as Aon’s outsourcing sale and Marsh’s from the deal with JLT, could also help to remove some of the negative pressures from lower organic growth moving forward, say analysts.