How insurance companies cede their risk and what region the reinsurance firm it is ceded to is domiciled in has been highlighted in some new data from the International Association of Insurance Supervisors (IAIS).

Globally diversifying risk is key to the success of the insurance and reinsurance markets, but patterns for cross-border reinsurance flows of risk differ greatly depending on the countries or regions involved.

In the 2016 edition of its Global Insurance Market Report (GIMAR) the IAIS takes a look at regional risk transfer patterns, using data from a survey of reinsurers with gross unaffiliated reinsurance premiums in excess of USD 800 million.

The survey looks at data from 2015 that was collected during 2016 and given the way the reinsurance market has been developing there are both unsurprising and perhaps surprising trends revealed in how regions cede their risks and where to.

The IAIS explains the importance of global risk transfer, saying; “Geographical diversification of risk is a key element of reinsurers’ risk management strategies. By ceding insurance risk across borders, jurisdictions exposed to catastrophe may benefit from a reduced concentration of insurance risk exposures within the borders of the jurisdiction. This can positively contribute to the financial stability of the jurisdiction.”

So it’s no surprise to see from the data that developing insurance markets, such as Africa and the Middle East, cede a significant proportion of their premiums to overseas reinsurers in regions such as Europe and North America.

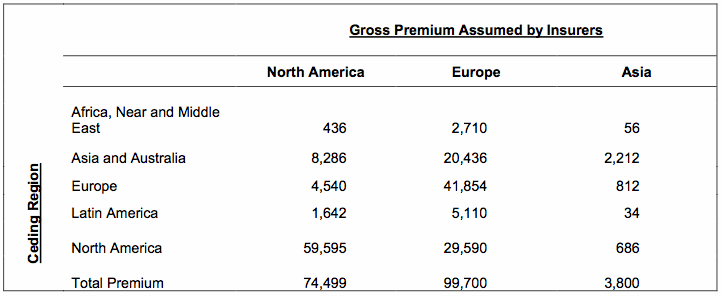

Gross premiums assumed by insurers and ceding region, year-end 2015 (USD millions) From the IAIS

As the above table shows, European reinsurance firms take the majority of risks ceded from Africa, the Near and Middle East. The regions reinsurers also take the bulk of Asia and Australian, and Latin American risks too.

This is unsurprising due to the four major European reinsurance firms, which are the most active in diversifying on a global basis and have footprints in all these regions with local representatives to be able to work closely with regional insurance firms.

But more surprising is the fact that European reinsurers back the vast majority of European risks as well, showing that in Europe the risk is actually not flowing out of the region very well and so not being globally diversified in the same way.

However, while the extent of the European risk concentration is surprising, the fact it is happening is not.

The major European reinsurers are so large, capital rich and have vast balance-sheets, so they are happy to diversify Europe on a country by country basis, taking on some concentration risk at the same time. Of course, given the perils that Europe is exposed to the concentration risk is not significantly high.

The capital models of the major European reinsurers allow them to reinsure most of the European risks and still remain profitable. Although it is worth pointing out that European property catastrophe reinsurance programs have been deemed under-priced for a few years now by many in the market, likely a result of this ability to assume local risks at the major players.

The North American market meanwhile does not keep as much of its risk at home, with Europe’s reinsurers assuming half as much as local reinsurers. Of course North America cannot compete on size of reinsurers, except for Berkshire Hathaway, so it does not have a concentration of four of the biggest players in the world at home to assume its risks.

One final point to consider is that some of the regional dispersion of risk could be hindered by cross-border rules for risk transfer. The recent agreement between the European Union (EU) and the United States (U.S.) to boost the $3 billion transatlantic insurance and reinsurance industry could lead to greater inter-regional reinsurance cessions in future.

But protectionism is of course also on the rise, in certain regions, and so this data could look quite different in years to come.