AM Best has estimated that global reinsurance capital levels will shrink by the end of the year.

A new note from the firm says that it expects to see a decline in overall available capital from its observation of the reaction of investment markets to interest rate hikes, continued inflation, and potential recession. Based on conservative estimates, it said, there may be a return to levels close to those of 2020.

A new note from the firm says that it expects to see a decline in overall available capital from its observation of the reaction of investment markets to interest rate hikes, continued inflation, and potential recession. Based on conservative estimates, it said, there may be a return to levels close to those of 2020.

It wrote: “Still, available capital growth has been aided by improvements in underwriting results, which reflect a re-alignment of most companies’ risk profiles toward more profitable and stable lines of business, the benefit of higher prices, and reduced exposures to property cat. We expect this to continue, even if inflationary pressures may squeeze some of those margins.”

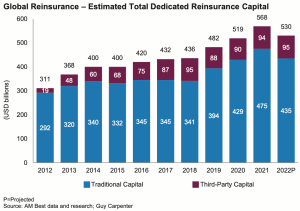

AM Best advised in its note that important distinctions still need to be made between ‘available’ and ‘dedicated’ capital, given that the former does not translate automatically into the latter.

It added: “The fact that available capital remains plentiful—over the last five years less than 85% was needed to support a BCAR (Best’s Capital Adequacy Ratio) assessment of “Strongest”— has fortunately not translated into lack of underwriting discipline. Reinsurers remain focused on stabilizing results and consistently working to meet their cost of capital—something that still constitutes a mixed bag. Given the current market uncertainty, most players feel the need to keep a material amount of dry powder to protect their balance sheets against market fluctuations and to deploy resources prudently when the right opportunities arise.”

Looking ahead, AM Best said: “Will the 2023 renewals mark a turning point for a “true” hardening market, able to attract new capital in droves and expand supply? Will third-party capital providers move first, as they have in previous cycles, taking advantage of the current retrenchment from traditional players and driving a new softening trend? Trying to predict the future is even more complicated nowadays, because how the year-end renewals go will depend heavily on actual claims activity and on where the global economy goes.”

It added: “If we have another active property catastrophe year—even one with no major catastrophic event, but an accumulation of several medium-sized ones as in the recent past—and inflationary pressures continue, combined with recession fears, uncertainty could remain so high that few investors will feel comfortable deploying capital regardless of the price. A few new entrants will still try, but their impact is likely to be limited in a market in which rates could continue to rise in response to more limited dedicated capacity.”