International Financial Reporting Standards (IFRS) 17 introduced a new way of financial reporting for insurers and reinsurers, fundamentally changing how they recognise and measure insurance contracts.

While this new standard promises greater transparency and comparability, it has also presented a significant challenge for industry participants.

While this new standard promises greater transparency and comparability, it has also presented a significant challenge for industry participants.

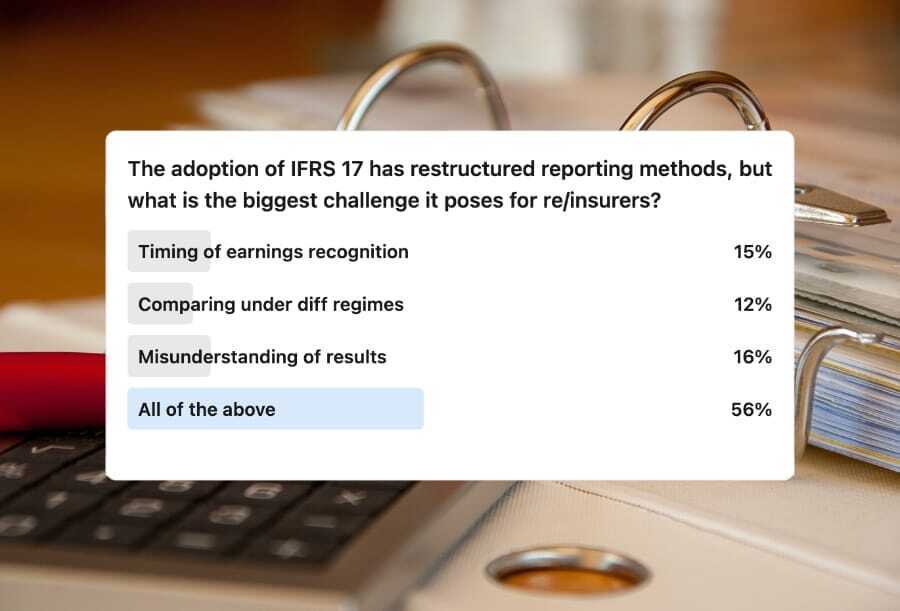

In a recent poll, Reinsurance News asked industry professionals about what they considered to be the biggest challenge the new reporting method brings for re/insurers.

The results revealed a widespread concern across the industry regarding the challenges posed by IFRS 17.

Of the hundreds of respondents to our poll, 16% see the potential for misunderstanding of results as the main challenge, while 15% believe it is timing of earnings recognition.

Only 12% selected comparing under different regimes as the main challenge. However, most (56%) of the respondents believe that all of these issues are what make IFRS 17 challenging, underscoring the need for clear communication and comprehensive guidance as the industry adapts to this new standard.

Launched in late 2023 amidst a historically challenging reinsurance market, IFRS 17 has overhauled previous methods for measuring and reporting insurance results and introduced new terminology, forcing re/insurance companies to adapt quickly.

Reinsurers traditionally relied on metrics like combined ratios and return on equity to assess performance. While still relevant under IFRS 17, these metrics are no longer directly comparable to US GAAP figures, making it harder to compare underwriting performance, especially against direct insurers.

While some believe substantial work is needed to better understand and explain IFRS 17, others believe it will be a positive change and create a lot of opportunity for reinsurers to help companies deal with the entwined disruption.

The introduction of IFRS 17 has undeniably shaken up the re/insurance landscape. While the industry acknowledges the potential benefits of increased transparency and comparability, the challenges associated with this new reporting standard are substantial.

Ultimately, the success of IFRS 17 will depend on the industry’s ability to adapt and communicate effectively.