Global property reinsurance prices increased sharply in 2023 on lower capacity, above-average catastrophe losses, higher inflation, and more financial and macroeconomic volatility, with analysts at DBRS Morningstar predicting tougher reinsurance market conditions to continue as the soft market is “decidedly over.”

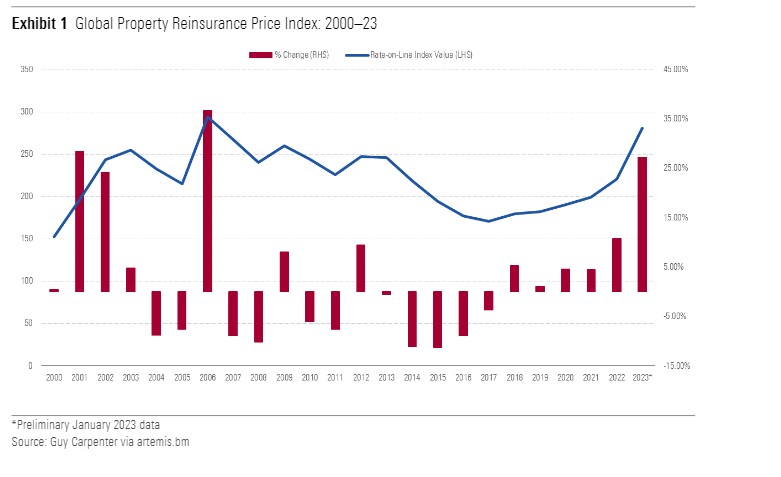

As noted by analysts, the last six years have seen increases in reinsurance prices, but none were as significant as the 27% increase recorded during the January 2023 property catastrophe reinsurance renewals, as highlighted by the Guy Carpenter Global Property Catastrophe Rate-On-Line Index.

As noted by analysts, the last six years have seen increases in reinsurance prices, but none were as significant as the 27% increase recorded during the January 2023 property catastrophe reinsurance renewals, as highlighted by the Guy Carpenter Global Property Catastrophe Rate-On-Line Index.

DBRS Morningstar explains that in the last 20 years, there was only one year when the price index was higher, and that was 2006, in the aftermath of Hurricanes Katrina, Rita, and Wilma.

Nadja Dreff, Head of Canadian Insurance, commented, “We expect the tougher reinsurance market conditions to continue in the short to medium term, putting to the test insurers’ risk management capabilities, which, if not adequate, could result in adverse credit rating implications.”

Analysts note that a confluence of factors are driving up prices, including the rise in interest rates in 2022 and subsequent material unrealised losses on investments reported by reinsurers. This industry-wide decline in total equities led to a reduction in reinsurance capital, ultimately impacting supply and pushing up pricing.

Of course, capital levels have since rebounded somewhat, and the higher interest rate environment is now contributing to better investment results. However, other factors are also pushing up reinsurance prices.

“For example, climate change continues to contribute to the escalating natural catastrophe losses that have been eroding reinsurers’ profitability year after year while also increasing the demand for more reinsurance capacity. Meanwhile, broad-based inflationary pressures continue to lead to a higher cost of claims as well as higher exposures.

“In light of these market conditions, reinsurance prices have continued to show firming in each of the property catastrophe reinsurance renewal periods throughout 2023,” explains DBRS Morningstar.

For insurers, the higher cost of reinsurance and tighter terms and conditions is happening at a time of increased demand for protection to navigate inflation and elevated losses from natural catastrophes, as well as emerging loss trends.

Analysts at DBRS explain that in light of these market conditions, insurers can either pay more for the same reinsurance program, restrict new business or exit certain lines / geographies, or adjust their use of reinsurance and strategy.

In terms of paying more for coverage, analysts warn that unless carriers can charge higher premiums to policyholders, this approach hinders profits, and the reality is that in some jurisdictions regulations make this difficult or impossible.

The most popular approach taken by insurers throughout 2023 renewals has been to adjust their reinsurance programs, notably to raise attachment points and in turn retain more risk. This approach has also been supported by the fact reinsurers have moved away from frequency risks and are more willing to participate higher up the tower.

However, a higher attachment point means that the insurer bears more risk, which analysts at DBRS Morningstar warn could increase income volatility and have a negative impact on credit ratings.

It’s an interesting time in the global re/insurance market, and with the hard market expected to persist into 2024, absent a significant inflow of new capital, which so far has failed to happen, it’s likely insurers will have to continue to explore their use of reinsurance in the months leading up to the January 2024 renewals.