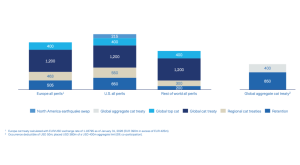

Synthetik Insurance Technologies’ recent report highlighted the potential for losses stemming from strikes, riots and civil commotion (SRCC) to spread across the UK, with some modelled scenarios exceeding £4 billion.

![]() The report takes the form of four trigger-based vignettes or modelled scenarios. These are based on protests surrounding asylum hotels in the UK in 2025 and represent four risks shaping UK SRCC exposure: local flashpoints; policing legitimacy; overseas conflict and domestic mobilisation; and macro-financial stress. The scenarios were modelled using Synthetik’s platform, srccQuantum.

The report takes the form of four trigger-based vignettes or modelled scenarios. These are based on protests surrounding asylum hotels in the UK in 2025 and represent four risks shaping UK SRCC exposure: local flashpoints; policing legitimacy; overseas conflict and domestic mobilisation; and macro-financial stress. The scenarios were modelled using Synthetik’s platform, srccQuantum.

Synthetik identified a surge in protest volumes stretching policing, transport and retail security, alongside the probability of marches tipping into opportunistic disorder, as structural and behavioural factors that can allow incidents to rapidly scale and evolve into multi-hub disturbances.

The report listed three key issues that carriers and brokers should be aware of, including that losses scale non-linearly when unrest routes converge near dense retail, policing and transit hubs. Therefore, routes and corridor exposure are vital to understanding worst-case loss outcomes.

Synthetik also highlighted that event duration can be as significant as severity, underscoring the need for disciplined event definitions and temporal aggregation awareness in SRCC underwriting.

In addition, regional towns represent a layer of accumulation risk, particularly in commuter belts.

Tim Brewer, Founder & COO of Synthetik, commented, “SRCC in the UK has evolved from a background peril into a route-based accumulation risk that is critical to monitor accurately. The severity and spread of loss depend on how civil unrest manifests across spaces, creating concentrations of exposure that may not be visible in more generalised approaches (e.g., concentric rings). For underwriters and brokers, this represents a significant change in how risk is priced, monitored, and accumulated across portfolios.”