European windstorm Friederike, which struck parts of Ireland and the United Kingdom before moving towards continental Europe where the impacts from the storm were seen as more severe, is expected to result in an insurance industry loss of between €1.3 billion (US$1.6bn) and €2.6 billion (US$3.3bn), according to catastrophe risk modeller, AIR Worldwide.

The majority of the insurance and reinsurance industry losses from the storm is expected in Germany, France, the UK, Belgium, and the Netherlands, with lower loss levels expected in Austria, the Czech Republic, Denmark, Estonia, Finland, Ireland, Latvia, Lithuania, Luxembourg, Norway, Poland, and also Sweden, says AIR.

The storm impacted parts of Europe between the 17th and 19th January 2018, causing damage to buildings with some reports that the storm’s winds were blowing roofs off buildings.

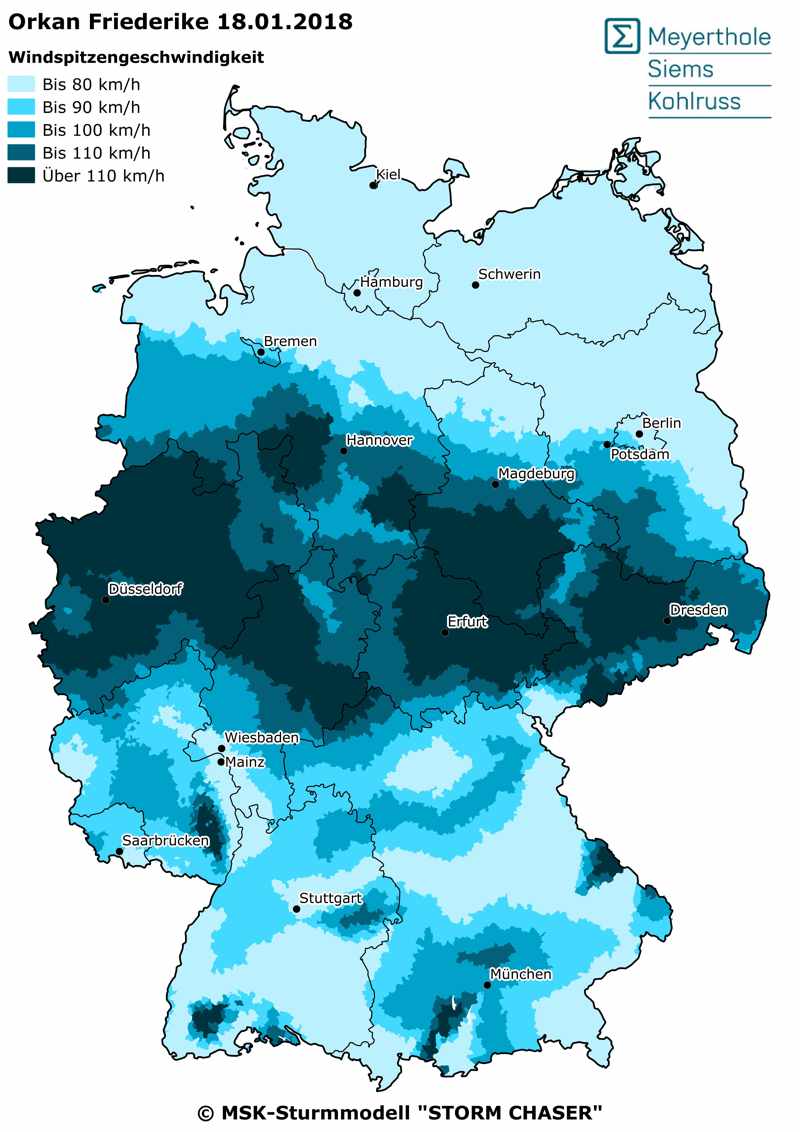

The UK was first hit by the storm, which bought wind gusts of up to 130km/h. In Germany, wind speeds exceeded 200km/h in mountainous regions, and reached almost 140km/h in low-lying areas, with actuaries suggesting previously that the storm could drive an insurance and reinsurance industry loss of as much as €800 million (US$1bn) in Germany alone.

Some 14,000 homes were left without power as a result of the storm, which caused widespread travel disruption across parts of Europe.

Deutscher Wetterdienst (DWD), a German meteorological service, has said that European windstorm Friederike is one of the strongest of the last 11 years, since storm Kyrill, although Kyrill was a considerably larger storm.

AIR’s insurance industry loss range for European windstorm Friederike only reflects wind damage to onshore residential, commercial, and industrial properties, and includes insured physical damage from wind to property, including structures, contents, and direct business interruption. The modelled loss estimate range also includes insured physical damage from wind to greenhouses in both the Netherlands and Denmark, and losses to insured forestry in Finland, Norway, and Sweden.

AIR explains that the modelled insurance industry loss estimate range does not include losses as a result of coastal or inland flooding, business interruption and additional living expenses for residential claims for all modelled countries, with exception of the UK. Furthermore, the modelled loss estimate range does not include losses to uninsured properties, losses to infrastructure, or demand surge.

The map below, from actuarial firm Meyerthole Siems Kohlruss (MSK), shows storm Friederike’s top wind speeds in Germany: