The April 1 reinsurance renewals saw a better alignment of client and reinsurer expectations in Japan in the casualty market, according to Gallagher Re’s 1st View report.

![]() For Japanese buyers, both client and reinsurers expectations were better aligned than at January 1, which led to a more orderly renewal process, the broker said.

For Japanese buyers, both client and reinsurers expectations were better aligned than at January 1, which led to a more orderly renewal process, the broker said.

This was aided by both the long-term nature of reinsurer relationships in the Japan market as well as the considerable improvements in primary underwriting that Japanese insurers have achieved in recent years.

The broker said that the casualty treaty market stayed “calm and logical”, similar to how it was on January 1. However, there is growing worry about the verdicts of US ‘nuclear’ awards on US casualty placements. This concern is also affecting some treaties that have incidental US exposures.

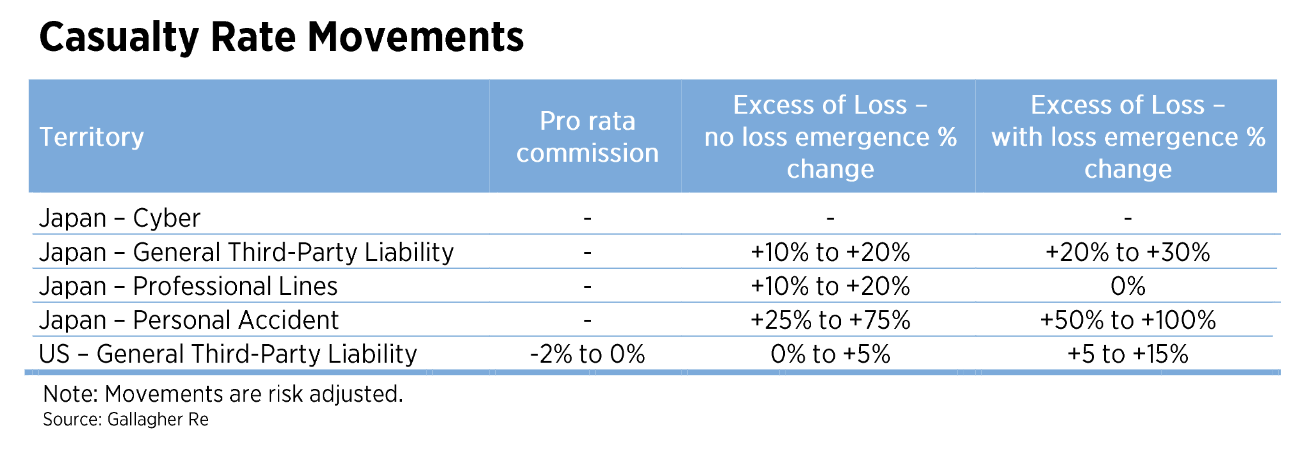

Japan, which is a central focus for the April renewals, saw primary rates stable in the cyber market, while coverage remained relatively restrictive by global standards. Reinsurers continue to find reinsurance purchases appealing as a way to diversify their portfolios, which results in a steady demand for this type of service, the report noted.

Gallagher Re noted insurers in Japan were interested in expanding their coverage beyond catastrophic events for third-party liability, but they were careful in how they allocated their resources due to worries stemming from loss events in the United States and related discussions. These concerns led to a cautious approach to capacity deployment.

The personal accident market, which has historically been quite stable, experienced disruption in 2022 due to significant losses related to COVID-19 that impacted several large personal accident programs, the broker noted.

Japan saw excess-of-loss (XoL) with no loss emergence in the range of 10% to 20% for general third-party liability, while XoL with loss emergence was upto 30%. In professional lines, XoL with no loss emergence was in the range of 10% to 20%, while XoL with loss emergence was flat. For personal accident the XoL with no loss emergence was upto 75%, while XoL with loss emergence was upto 100%.

The broker said overall dynamics for US third-party liability remain stable due to “continued strong appetite by US reinsurers for US casualty.”

US saw excess-of-loss (XoL) with no loss emergence upto 5% for general third-party liability, while XoL with loss emergence was upto 15%.