Global reinsurance market survey – H2 2021

Reinsurance market survey – H2 2021

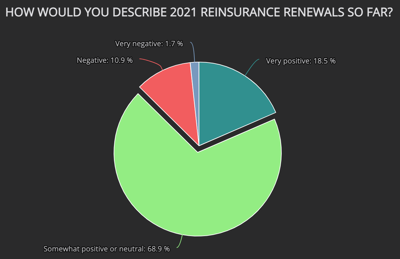

Respondents to our latest reinsurance market survey, in collaboration with sister-site Artemis, are optimistic for further rate hardening at the important January 1st 2022 renewals, as pricing remains the key for buyers of protection.

Data from the 2021 edition of the global reinsurance market survey is based on responses from hundreds of identifiable market participants, of which more than 70% make or provide input into reinsurance buying decisions.

Data from the 2021 edition of the global reinsurance market survey is based on responses from hundreds of identifiable market participants, of which more than 70% make or provide input into reinsurance buying decisions.

With the Jan 2022 reinsurance renewals fast approaching, against a backdrop of elevated catastrophe losses, fading but still impactful COVID-19-related losses (notably within life and health), greater demand, and a continuation of underwriting discipline, we wanted to test the temperature of the international reinsurance sector.

The full results are available online for free and you can analyse the data from responses here.

The survey shows that market participants are anticipating the most dramatic rate increases within loss-affected lines of business, notably U.S. and European property cat risks, reflecting the impacts of winter storms and hurricanes in the U.S., and devastating flooding and flash floods across parts of Europe.

Outside of the property cat arena, more than 50% of survey respondents are expecting rates in the cyber market to increase by at least 10% at the upcoming renewals, with optimism for meaningful rises also evident in professional lines, retrocession, and political risks.

Alongside pricing, credit quality / rating, and reputation are the main aspects buyers of protection are looking for in a reinsurance counterparty, while reduced control / exposure, earnings protection, and capital efficiency / relief are viewed as the main drivers of purchasing decisions at 1/1 2022.

Throughout this year, reinsurers have noted greater demand for protection and heading into the renewals, approximately 92% of buyers expect to purchase roughly the same or more reinsurance or retrocession protection.

It’s a similar story for the use of alternative, or third-party reinsurance capital, with the large majority of survey respondents expecting to leverage about the same or more insurance-linked securities (ILS) backed capacity.

Although the COVID-19 pandemic is by no means behind us, the relaxation of strict restrictions in many parts of the world as the global vaccine rollout continues, coupled with a focus on exclusionary language within policies, has seen the cost of the pandemic fade across the industry.

While this is clearly evident within property and casualty lines of business, still elevated mortality rates in some countries means that for some reinsurers, COVID-related losses on the life and health side of the business remain and continue to exceed expectations for some.

Of course, a pandemic isn’t the only systemic risk that threatens to challenge the global reinsurance industry, and considering the sector’s response, almost half of survey respondents feel that despite some positive signs, they’re slightly concerned about the market’s ability to navigate future challenges of a similar scale.

Promisingly, however, less than 7% of respondents feel less confident than ever in the reinsurance market’s ability to weather such a challenge in the future.

Additionally, survey respondents offered their thoughts on the potential for mega-M&A deals to complete as global competition and antitrust concerns increase.

The data also shows that looking forwards, market participants are split on how positive the outlook is for the sector with climate change, cyber risks, and rising losses from secondary perils seen as the greatest challenges to profitability over the next five years.

But with challenge comes opportunity, and as the data shows, market players are eager to prioritise technology, diversification, and the fostering of talent and acquiring expertise as we head into 2022.

We’ve made the full results of this global reinsurance market survey freely available to our readers and we’re happy to discuss the results with industry participants and to discuss sponsorship enquiries from those looking to raise their profile in the reinsurance sector. Contact us.

Getting your daily reinsurance news from Reinsurance News is a simple way to receive only the reinsurance industry news that matters, delivered directly to your email inbox.