InsurTech start-ups have continued to record robust premium growth so far in 2018, however, generating a sustainable loss ratio below 100% remains a challenge, according to analysis by two industry executives.

A recent article co-authored by Adrian Jones, Head of Strategy & Development at reinsurance giant SCOR, and Matteo Carbone, Founder & Director of IoT Insurance Observatory, a global industry think tank focused on the Internet of Things in insurance, explores the performance of a number of InsurTech companies in the second-quarter of 2018.

One of the interesting points highlighted by the pair, is the fact InsurTech start-ups are outperforming industry veterans on premium growth, but falling short on loss ratios, which, despite being “generally stable or improving slightly”, remain “unsustainable.”

“Premium growth continues to be robust, but loss ratios generally remain at/above 100% for the start-ups in our analysis,” said Jones.

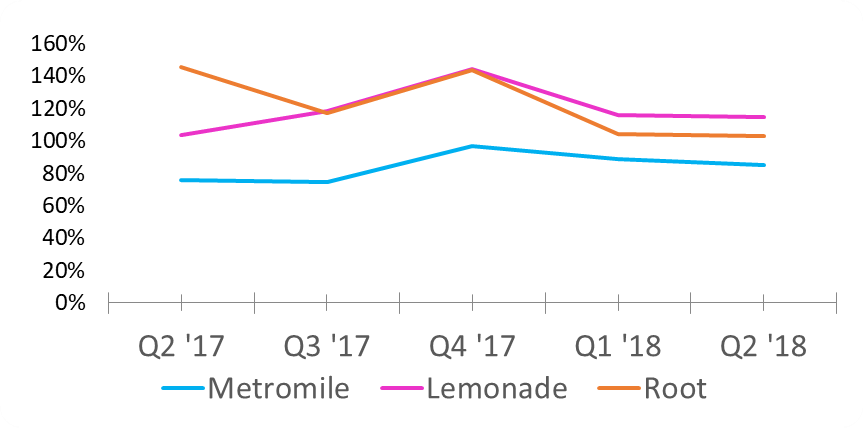

The three independent P&C InsurTech start-ups discussed are Lemonade, Metromile, and Root. The chart below, provided by the co-authors, shows the gross loss ratio evolution of the three venture-backed start-ups.

As shown by the above chart, the gross loss ratios for the three companies in Q2 remain relatively unchanged from the previous quarter. The experts note that both Lemonade and Metromile experienced adverse development in Q2, which increases the reported loss ratio.

“If our subject companies are shifting management attention towards profitability, it is not yet obvious in the figures. Improving underwriting results is like steering a slow-moving boat. You can turn the tiller, but the boat may not go the way you want, and it will take some time. Insurance policies last a year, rates are regulated by states, and unsettled old losses can get worse if the legal environment changes,” explains the article.

According to the pair, Metromile’s reported figures have always shown the most profitability, and the firm also managed to reduce its gross loss ratio by 4 points in Q2.

The gross loss ratios for all three companies have clearly been trending downwards since the fourth-quarter of 2017, but continue to remain at or above the 100% mark. Eventually, warns the pair, gross loss ratios “need to be sustainable,” with gross being before any premiums and losses are passed on to reinsurers, which the article says “isn’t a sustainable long-term strategy.”

During Q2, the gross loss ratio for Lemonade was 120%, for Metromile 95%, and for Root, 112%. For the net loss ratio, these figures change to 71%, 107%, and 96%, respectively. While the ceded loss ratios in Q2 totalled 361%, 86%, and 143%, respectively.

Despite the warnings, unsustainable loss ratios are not an issue for all start-ups, says the article, although noise at industry events is increasingly focused on profits and not just growth.

“We welcome these signs of maturity in the InsurTech market, which were a big reason we started writing these articles and presenting at conferences,” says the pair.

The data shows that when compared with industry veterans, InsurTech start-ups are struggling to produce and maintain sustainable gross loss ratios. However, premium growth continues to be strong, despite the article revealing that for two of the three companies discussed, premium growth in Q2 was actually the slowest of the last five quarters.

Direct premium growth at Lemonade was 32% in Q2, which is down from the 63% recorded in Q1. For Root it is a similar story, with the company recording direct premium growth of 88% in Q2, compared with 205% in Q1. Metromile grew its direct premiums by 6% in Q2, which is down from the 25% recorded in Q1, but up on the 3% premium growth witnessed in Q4 2017.

The article goes on to highlight that robust, but slowing premium growth might be in response to seasonal effects, as well as the fact early adopters of direct insurance may have already been won; it might be harder to sell the value proposition that was previously expected; retention rates might be lower than expected; and, that companies are focused on state expansion and team growth.

The article also highlights a counter-point, that InsurTech companies could be growing faster but instead are focused on profit rather than rapid expansion.