The report “Decrypting AI for Insurance” written by Swiss Re’s Group’s Chief Digital & Technology Officer, Pravina Ladva has outlined ways in which AI could help achieve the industry’s long-term goals and takes a deep dive into the immediate benefits of AI that can be taken into consideration.

Ladva tries to reimagine AI when it comes to the re/insurance industry as a tool for the future that will potentially enable more precise coverage and pricing adjustments. While this is an attractive long-term goal, the report discusses AI is delivering benefits today and the opportunities for the insurance value chain in the near future.

Ladva tries to reimagine AI when it comes to the re/insurance industry as a tool for the future that will potentially enable more precise coverage and pricing adjustments. While this is an attractive long-term goal, the report discusses AI is delivering benefits today and the opportunities for the insurance value chain in the near future.

AI refers to mathematical models that learn patterns from data and enable faster or even automated decisions.

Swiss Re defines AI into various categories, depending on its scope, AI can be referred to as either “narrow-AI” which means a model designed to fulfil a specific purpose in a defined context or “general-AI” which is defined as a universal model with human-like intelligence.

According to Ladva, “No true general-AI exists yet, but recent advances partly begin to exceed capabilities associated with narrow-AI (e.g., Open AI’s ChatGPT and GPT-4 or Google’s Bard). Current insurance AI applications are based on a narrow type of Artificial Intelligence.”

Narrow-AI is already being used in many industries although in insurance, it has three main functions. First, it can be used to automate repetitive knowledge tasks like classifying submissions and claims. The second is that it can generate insights from large complex data sets to augment decision-making which means it can help with portfolio steering and risk assessment. The third is that it can enhance parametric products and risk solutions.

Ladva cautions that although AI enables re/insurers to become more efficient and offer new solutions, it’s important to keep in mind that, so far, an entire system is required for its use, including human interaction. The added value of AI therefore only comes from the smart combination of AI models and human processes, not just a standalone AI model.

The AI technologies most leveraged in insurance today are Machine Learning, Natural Language Processing, and Computer Vision. Advanced analytics, and some forms of AI, have been increasingly enriching the insurance value chain for several years and will have a different impact on each stage of the value chain in the future.

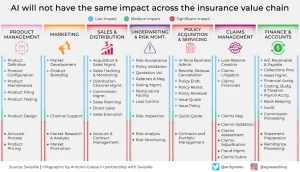

“AI will not have the same impact across the insurance value chain. The report showcases the example of three areas in which AI can be used in insurance. While underwriting, AI can help improve risk assessment and customer understanding. Re/insurers get access to endless amounts of data at the time of underwriting due to the digitalisation of existing touch points or access to new data assets with digital partners like telematics, remote sensors, satellite images or digital wellness records. The ability of re/insurers to convert this data into actionable insights for underwriting, is a key competitive differentiator, as it allows them to offer customers more tailored coverage and pricing,” said Ladva in the report.

AI techniques such as supervised learning can complement and streamline certain UW processes when it comes to smarter triaging and routing. AI-driven predictive models at Swiss Re support triaging Life & Health underwriting and simplify the consumer journey.

The report presents claims as the second avenue for AI where it can help improve back-end processes, new products, and coverage for more risks. AI capabilities can improve efficiency and insights and also enable the development of new solutions and coverage for previously uninsurable risks.

Swiss Re’s parametric Flight Delay Compensation is built on an AI model that can predict flight delays. In the event of a delay, customers who purchased the insurance when buying their ticket will receive an instant payout without having to file a claim. The solution uses more than 200 million historical data points and the machine-learning capability of the pricing engine allows for rate adjustments, based on data from over 90,000 flights per day.

The third avenue is, claims that it can help with computer vision that can reduce car accident fraud and detect driving style. Taking advantage of the confluence of edge computing and AI, an Italian startup has been granted a patent to record the front visual panorama of a moving vehicle, identify the driver’s driving style, and certify the accident by recording its dynamics.

When the engine starts, the device begins recording the video and simultaneously transmits it to the cloud using proprietary technology that allows secure transmission of encrypted video snippets. Once in the cloud, the video snippets are reassembled and processed using computer vision algorithms that anonymise the personal data collected during the recordings (such as people’s faces and car license plates) to comply with data privacy regulations (e.g., GDPR). The anonymised video can then be used as evidence of accident dynamics and to extract key data to identify driving styles and the ability to classify driver risk. The system has received funding from the Italian government to develop part of the project.

The report shows a few examples of data-driven AI models that have been successfully deployed. However, at Swiss Re and across the industry, many AI projects are also internally driven and address core processes like using natural language understanding to help ingest and classify unstructured data into decision-making processes or to better understand the exposure in contracts and the overall portfolio.

“Though AI has the potential to impact and add value to the entire insurance it also comes with wider access to these powerful tools, it is also crucial to be on top of their risks and challenges. Data and responsible AI literacy are key for companies to ensure that humans remain in control of the decision-making process. There are many new risks associated with the use of AI at a scale that policymakers, big tech companies and insurance companies need to consider working on now so that AI adds value to society and that we can still effectively protect against the new risks associated with it,” added Ladva.