The latest edition of the REDY Index by CRC Group reveals that Q2 2024 continues the positive trends in the E&S property market observed over the past two quarters.

These developments suggest a turnaround from the challenging market conditions witnessed in Q2’23.

According to CRC Group, E&S property carriers now have increased confidence in their portfolios, reinsurance limits, and costs.

Carriers are actively seeking growth in premiums and exposures while adjusting pricing targets. This strategy has allowed clients to secure higher limits, harmonise terms and pricing across placements, and often achieve significant rate decreases.

Although the broader market has experienced a slowdown in rate increases, specific micro-markets still face difficulties influenced by factors like location, property valuations, and claims experience.

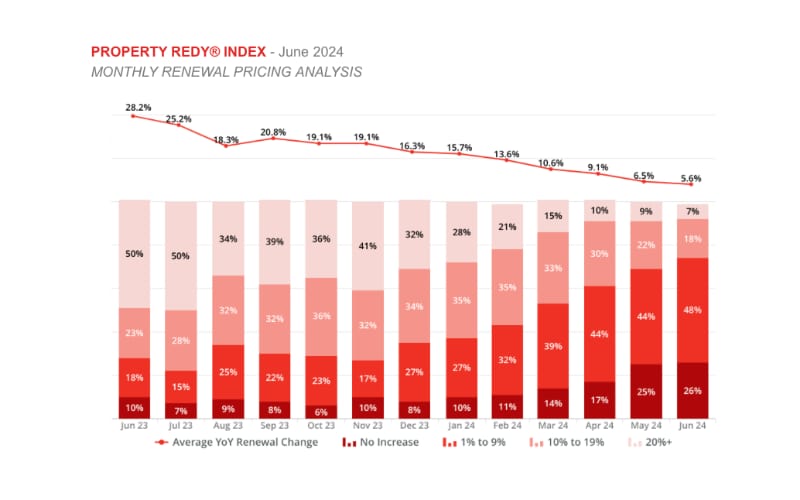

As you can see from the chart below, which shows pricing trends based on average property renewal premium on a broad range of accounts in all 50 states, deceleration is evident.