Reserve releases are expected to continue to bolster the results of North American insurers and reinsurers over the next two years, albeit at a lower rate than previously and with fewer firms expected to benefit as redundancies fall further, according to analysis from Keefe, Bruyette & Woods (KBW).

Throughout the soft reinsurance market cycle reserve releases have often been a focal point of discussion, driven by aggressive reserving practices by some re/insurers in an effort to offset persistent underwriting and investment return declines.

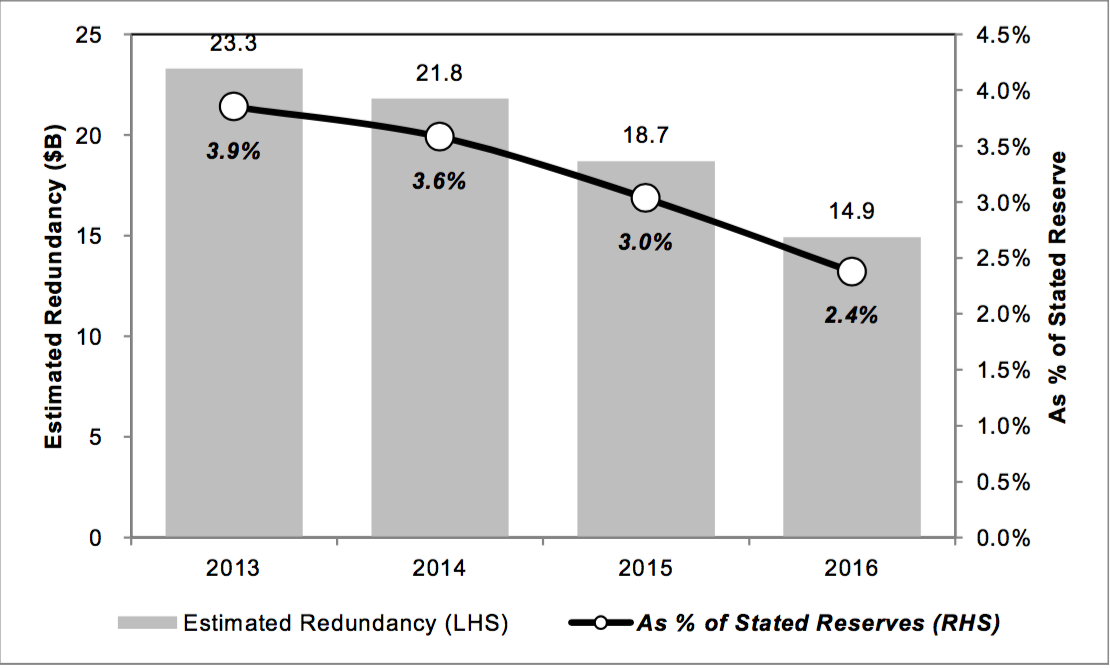

KBW notes that reserve redundancies continue to decline across the property and casualty (P&C) industry, as shown by the below chart, which analysts attribute to the decelerating rate increases and/or rate decreases in recent years.

“We still expect reserve releases to augment underwriting results in 2017 and 2018, but to a lesser extent – and probably for fewer insurers – than in recent years,” says KBW, in a recent note on the reserve environment of the North American P&C industry.

Analysts also explain that as at the end of 2016 the U.S. P&C sector’s overall statutory loss and defence and cost containment reserves were overstated by approximately $14.9 billion, compared with an estimated $18.7 billion a year earlier.

The majority of reserve redundancies in most business lines were “modestly offset” by deficiencies in commercial auto liability, product liability, and other liability business lines, says KBW.

Overall, KBW expects “recent calendar years’ trend of declining releases to persist.”

With reserves expected to fall further in the coming months and the insurance and reinsurance industry remaining under significant pressure, in terms of investment and underwriting return metrics, it will be interesting to see how profitable companies are in the months and years ahead absent the ability to release higher levels of reserves, ultimately bolstering returns and masking true underwriting profitability.