Analysts at Kroll Bond Rating Agency (KBRA) anticipate that large capacity reinsurers are set to begin retaking market share as pricing conditions harden.

Despite top-line growth, KBRA sees these players as overcapitalised and ready to reclaim business they may have given away during the soft market.

Going forward, the firm expects to see moderate capital repatriation in the form of dividends and share buybacks, although further top-line growth will largely depend on the amount of capital still available.

In the past few years, market conditions have made it difficult for larger reinsurers to invest excess capital into growth, but analysts argue that positive market sentiment has now translated into larger appetites.

This is particularly true among reinsurance market leaders, they said, albeit not at a scale that could materially reduce excess capital.

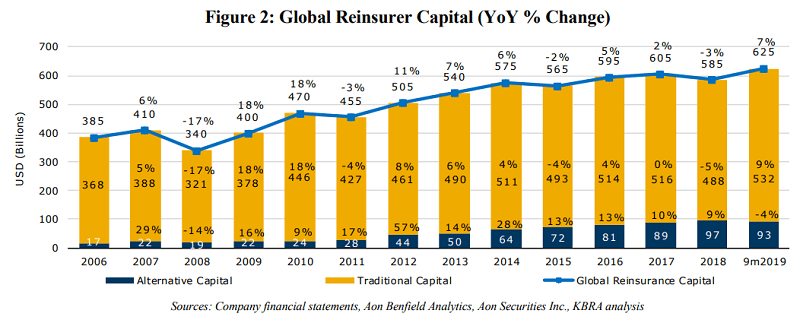

Global reinsurer capital was up 7%, to reach $625 billion in the first nine months of 2019, as traditional

capital benefitted from a favourable market environment that supported investment gains.

According to Willis Re Securities, traditional capital increased 9% to $532 billion, which offset a 4% alternative capital decline to $93 billion.

But while general market sentiment at during the recent January renewal period was positive, there does seem to be a sense that reinsurers were somewhat disappointed by the extent of price firming.

For example, while the overall pricing environment is positive, prices in non-proportional business are only back at levels seen in 2011.

Low interest rates are also a persistent problem for both primary insurers and reinsurers, although KBRA does not consider the resulting earnings pressure to be a credit negative, and has in fact seen underwriting discipline improve as rates fall.