The UK government has announced it will be introducing secondary legislation to give effect to the planned Solvency II reforms, the prudential regulatory regime for insurers, at this year’s Autumn Statement.

According to the announcement, this will deliver a more tailored, clearer, and simpler regulatory regime for the insurance sector, and incentivise private investment in long-term productive assets, such as infrastructure.

According to the announcement, this will deliver a more tailored, clearer, and simpler regulatory regime for the insurance sector, and incentivise private investment in long-term productive assets, such as infrastructure.

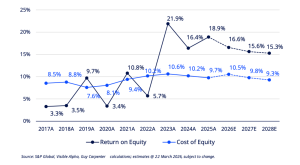

The proposed reforms – announced at Autumn Statement 2022 – are expected to alleviate capital strain and enhance Solvency II ratios for these insurers.

A view shared with a number of analysts, like J.P. Morgan, who have highlighted the positive impact these changes could have on UK life insurers, particularly those involved in Pension Risk Transfer (PRT) and annuity writing.

Others, like Ross Evans, Life Insurance Partner at PwC UK, highlight the uncertainties that still surround the implementation of the proposed reforms.

Evans commented: “While the Government has reaffirmed its plans to legislate for the Solvency II reforms, insurers will be left wondering when these changes will be enacted into law. The Government had set out a 31 December 2023 timeline to implement the proposed changes to the Risk Margin and release capital from UK insurers’ balance sheets. The lack of specificity on timing will increase uncertainty within the insurance industry on whether these changes will be enacted this year.”

He added: “The Government’s ambition is that the Solvency II reforms will help to incentivise £100bn of additional investment in UK productive assets over the next decade. The impact of the reforms is, however, yet to be seen and will also depend on the outcome of the current Prudential Regulation Authority (PRA) consultation on the Matching Adjustment (MA).”

The PRA announced its consultation on a significant package of reforms to the MA back in September.

According to the Authority, the proposals cover reforms to MA regulations relating to greater investment flexibility and revised eligibility rules and more flexibility in MA processes, along with risk management enhancements, a greater role for senior manager responsibility including through attestations, and certain changes to MA calculation and reporting.

Additionally, the proposed reforms are to “improve insurers’ investment flexibility by enabling broader and quicker investments by insurers in their MA investment portfolios, while supporting the PRA in holding insurers to account for managing the additional risks involved, through a range of proportionate supervisory measures,” the PRA added.