Re/insurance broker Aon has warned that secondary perils are accounting for an increasingly significant portion of global catastrophe losses and pose notable challenges for insurance and reinsurance companies.

While tropical cyclones often attract the most focus given the high financial toll that landfalling events can cause, losses from secondary perils cannot and should not be ignored, Aon said.

Individual financial losses from severe convective storm, flooding, wildfire, winter weather, European windstorm, and drought may not frequently carry the same eye-watering loss figures as hurricanes, but the accumulation of these smaller losses is a problem.

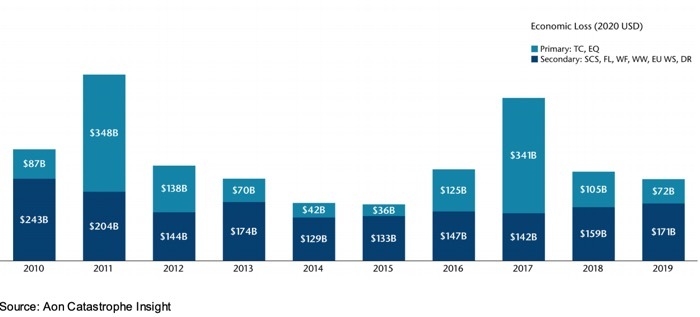

In fact, Aon notes that the relationship around primary and secondary perils is evenly spread on a global basis when looking at the overall economic damage costs.

Analyzing global economic losses, eight of the past ten years have featured secondary perils aggregating to higher financial costs than primary perils globally.

Only 2011 (major earthquakes in Japan and New Zealand) and 2017 (Hurricanes Harvey, Irma, and Maria) featured tropical cyclone and earthquake damage costs that surpassed the secondary ones.

And in Australia, secondary perils such as hail, inland flooding, bushfires and East Coast Lows have accounted for more than 74% of aggregated losses since 1967, while primary perils such as tropical cyclone and earthquake only account for 26%.

“The magnitude and consistency of losses from secondary perils makes it clear that properly understanding and managing the risk is an important key to controlling loss volatility and protecting earnings,” Aon stated.

“To do this, however, the right tools must be in place. An interesting observation from the modeling perspective is the disconnect between insurance penetration for individual secondary perils and industry investment in analytics tools to support those perils.”

Looking at the US specifically, tropical cyclones continue to be the costliest peril for the re/insurance industry, but Aon observes that the gap between tropical cyclones and the second costliest peril – severe convective storm – is not as large as is often assumed.

For example, since 1990, tropical cyclones have triggered $362 billion in cumulative losses by public and private insurers by comparison to severe convective storms at $330 billion.

The situation is very different for US inland flood, which has caused huge economic losses in recent years, but for which there is still a major lack of insurance coverage, with more than 90% of homeowners thought to have no coverage.

Insurance coverage for wildfire, meanwhile, falls somewhere between severe convective storms and inland flood, although there remains significant underinsurance in some key risk areas such as California.

Given the huge wildfire losses over the last several years, Aon notes that wildfire is emerging as an increasingly key risk for some insurers, having previously been eclipsed by earthquake in the western states and myriad other perils elsewhere.