Broker Howden expects to see continued demand for reinsurance into 2022 and the North Atlantic hurricane season after property-catastrophe reinsurers lacked the usual clarity on their net positions when offering lines at 1/1, amid late retrocession placements.

Alongside the late retro experience, Howden forecasts that continued purchasing interest through 2022 will be driven by S&P’s updated catastrophe charge methodology.

Among other things, S&P proposes to replace the flat 1-in-250-year post-tax property catastrophe capital charge with a pre-tax natural catastrophe (across all non-life business lines) capital requirement that varies from 1-in-200 to 1-in-500 years at different stress scenarios.

The proposed change means that certain insurers and reinsurers would need to potentially hold more capital, which in turn could lead to more demand for reinsurance and retro.

Overall, the January 1st, 2022 reinsurance renewals season has been described as mixed, bifurcated, challenging, and late.

Of course, some markets performed better than others but given the above-average catastrophe experience and subsequent elevated loss costs in 2021, property-catastrophe reinsurers were hopeful of some meaningful rate increases.

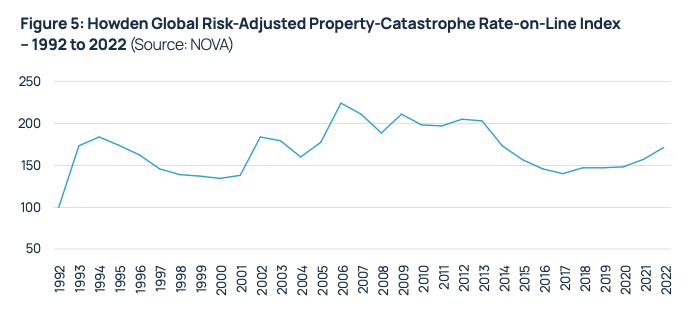

Globally, risk-adjusted property-catastrophe reinsurance rates-on-line spiked by an average of 9% at the Jan 1st, 2022 renewals, against 6% last year, finds Howden.

In fact, the broker concludes that this is the biggest year-on-year increase since 2009 and takes the index back to pricing levels last seen in 2014.

With the January renewals skewed to European programmes, the loss experience in the region throughout 2021, notably the flooding in July in Germany and neighbouring countries, “was a key inflating factor” notes Howden.

“Not only did the floods and storms in Germany and surrounding countries elevate losses in the region beyond previous highs, they also served as a reminder of the level of risk in parts of Europe following years of benign loss activity and price reductions.”

As a result, it’s been reported that some European catastrophe business saw rate increases of more than 50% at 1/1, with programmes in loss-affected territories typically seeing double-digit rises overall, on a risk-adjusted basis. Whereas in unaffected regions, pricing was flat to up modestly.

“A desire from capital capacity providers to achieve perceived pricing adequacy for lower-attaching perils led to more disciplined underwriting and higher attachment points across a number of programmes in Europe,” says Howden.

A persistent rise in losses from secondary perils and the uncertainty caused by climate change has led to an expectation of more frequent events, which in turn hindered the willingness of carriers to offer aggregate capacity.

The shift to per event, or occurrence capacity being more widely available was one of numerous changes to structures at the renewals, including higher deductibles, reports Howden.

In the U.S., “differentiation was a key feature”, says Howden, with lower layers exposed to the frequency of mid-sized losses witnessing significant pressure and restructuring to reflect the loss dynamics.

“Less acute tensions for higher layers helped cap overall risk-adjusted rate increases to mid- single-digits,” notes the broker.