Property catastrophe pricing has been mixed for reinsurers in Florida at mid-year renewals, as increased demand for some companies following 2017’s catastrophes was offset by further non-traditional capital entering the market, according to reinsurance broker Willis Re.

Willis Re’s 1st View Report observed that companies that performed well in Hurricane Irma were in high demand and had the largest amount of capacity at their disposal, with claims handling and underwriting emerging as key areas for renewal discussions.

Overall limit purchased in the market was also slightly higher than in 2017, although this was muted by an abundance of new capital entering the market, with non-traditional reinsurers offering larger lines and focusing more on reinstateable layers.

Many reinsurers were also required to restate their projected ultimate estimates for Hurricane Irma as issues with assignment of benefits and reopening claims caused loss creep to erode their positions.

Meanwhile, quota share renewals faced downward pressure on ceding commissions, which Willis Re attributed to a deterioration in underlying loss ratios and increased catastrophe activity.

The pricing environment in Florida was generally reflective of the larger U.S property treaty market, which experienced a supply/demand imbalance that resulted in mostly flat rates, with decreases even observed for pricing on some loss free layers.

Capacity also remains plentiful nationally, with non-traditional and collateralised markets increasing the amount of available capital and causing traditional reinsurers to defend their held portfolios and forego rate increases.

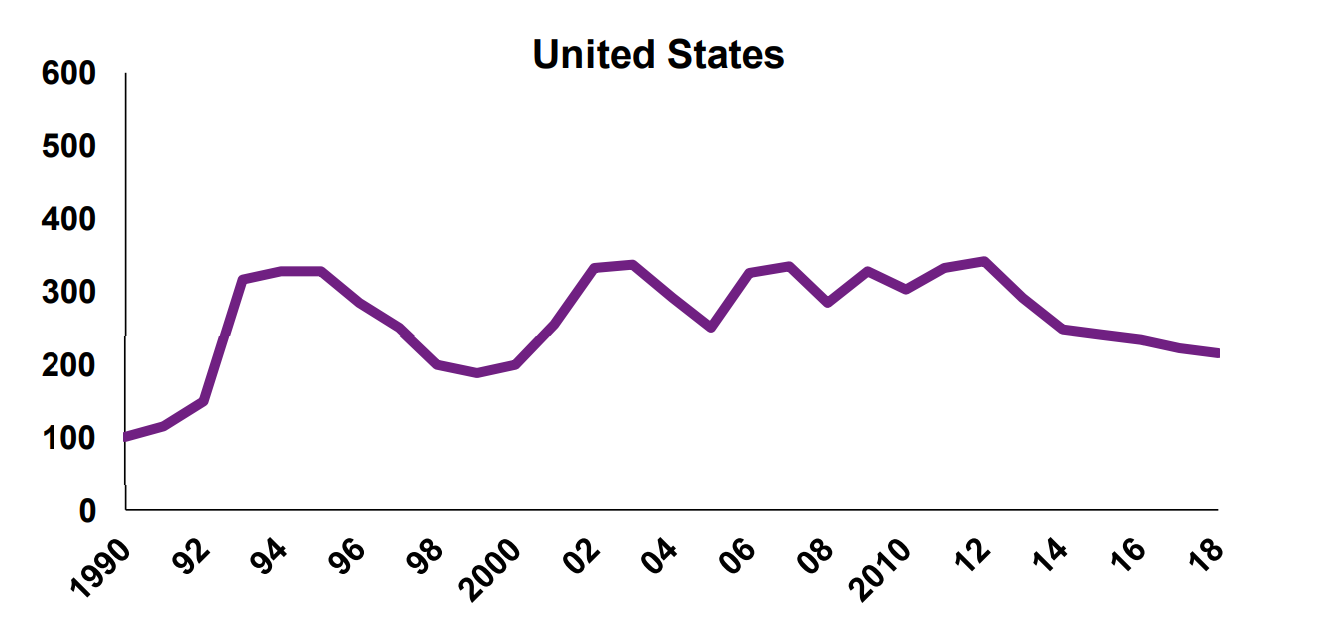

The below chart from Willis Re’s report shows that property catastrophe rates for reinsurers in the U.S have been declining fairly steadily for several years now.

Other loss hit areas, such as the Caribbean (including Puerto Rico) fared slightly better, with a wide range of risk adjusted terms increasing by 10% to 40% on excess of loss programmes, depending on the island and the extent of loss.

Additional capacity is also still available in the Caribbean market, while Hurricane Maria losses continue to increase as further business interruption losses emerge, although they remain below the originally modelled estimates.

Willis Re observed similar trends for most property catastrophe reinsurers globally, with abundant capacity causing reinsurance rates to remain flat or result in just mild increases.

Exceptions include certain reinsurers in Latin America who were exposed to Mexico earthquake losses. Rate increases for these layers increased up to 15%, although overall program increases were generally more muted at 2.5% to 7.5%.

In countries such as the UK, Willis Re noted that many major insurers were not adversely impacted by the 2017 storm activity, resulting in flat pricing and broadly consistent year-on-year purchasing behaviour for catastrophe treaties.