A myriad of events came together and drove the hardest property catastrophe reinsurance market in a generation at the key, January 1st, 2023, reinsurance renewals, with structures and coverage terms at the forefront of negotiations, according to re/insurance broker Howden.

The coalescence of geopolitical and macroeconomic shocks, the ongoing war in Ukraine, challenged energy markets, 40-year high inflation, rising interest rates, Hurricane Ian, and demand-side pressures at a time of depleted capital, has created a “highly challenged and complex reinsurance renewals at 1 January 2023,” notes Howden in its The Great Realignment renewals report.

For the property catastrophe space specifically, Howden says that both structures and terms were prominent in negotiations, driven by a recognition from all sides that prices would rise significantly on the back of recent loss trends, exacerbated in 2022 by Hurricane Ian and other loss events.

“Reissued firm order terms, non-concurrent terms and diversification plays leveraging demand for catastrophe capacity as a way to improve access and margins for non-property business reflected shifting market conditions,” says the broker.

Within property cat, late or incomplete retrocession placements ensured that property cat reinsurers had less clarity than usual around their net positions when offering lines at 1/1, which contributed to the late renewals.

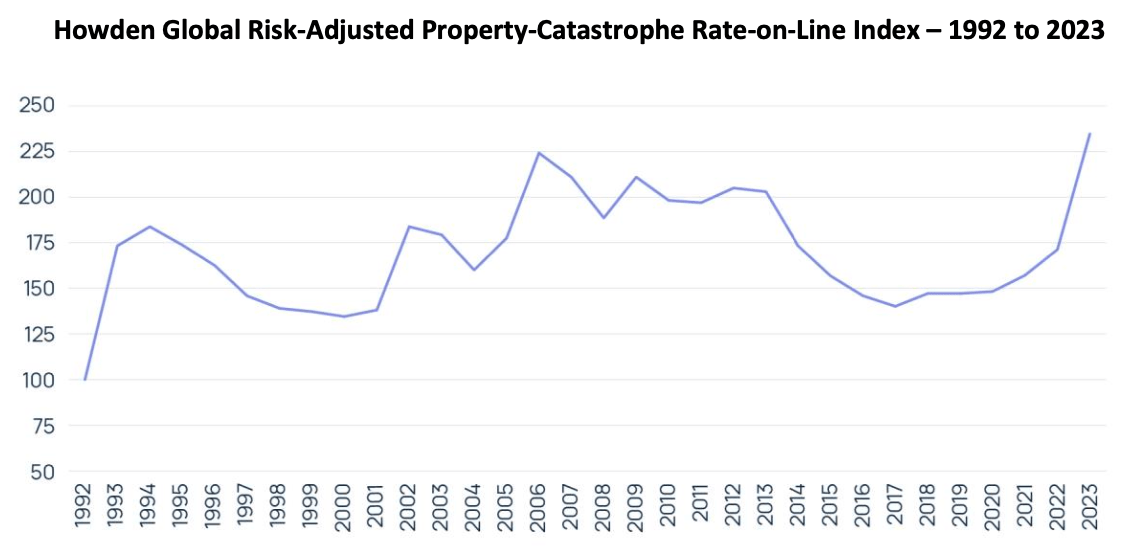

Howden says that its Global Property-Catastrophe Risk-Adjusted Rate-on-Line Index rose by an average of 37% at 1/1 2023, which is far higher than the 9% seen last year, and actually marks the biggest year-on-year increase since 1992, when the market felt the impacts of Hurricane Andrew.

In the European market, which experienced further damaging cat losses in 2022 after the impacts of storm Bernd in 2021, sellers of protection experienced strong demand for additional limits to counter inflation, which combined with some retrenchment from incumbent reinsurers, resulted in a difficult market environment for certain buyers.

In many instances, this led to higher attachment points, tighter terms, paid reinstatements and substantial rate rises, which were up 30% on average, but far higher for loss-hit programmes.

Importantly, however, Howden explains that capacity “was nevertheless sufficient to see most deals over the line, particularly for cedents able to demonstrate strong performance and / or leverage long-standing relationships.”

In the U.S., which experienced the impacts of Hurricane Ian in 2021 – poised to be the second costliest cat event in the market’s history – Howden says that the renewals were more challenged, with an average rate-on-line increase of 50%. In the U.S., this was the biggest change in rates-on-line since 2006, says the broker.

“Increased demand coincided with supply constraints to create the most difficult U.S. renewal in decades,” says Howden.

In fact, some buyers failed to fill their programmes at 1/1, while named-peril coverage was more prevalent. As a result, Howden reports that certain insurers resorted to shortfall covers.

In the retro market, Howden notes that Ian’s impact on an already dislocated market meant that a large portion of collateralised retro was trapped heading into 1/1 2023. All in all, risk-adjusted retro cat excess of loss rates-on-line increased by 50% on average, with a range of 20% to 90%.

David Flandro, Head of Analytics, Howden, commented: “The reinsurance sector has reached concurrent secular and cyclical tipping points. It is experiencing sustained, heightened loss activity and war risk just as the global economy exits the ‘great moderation’ of interest rates and asset price volatility. Pursuant increases in carrier costs of capital are underpinning higher rates-on-line, lower capacity levels, and straitened terms and conditions.”

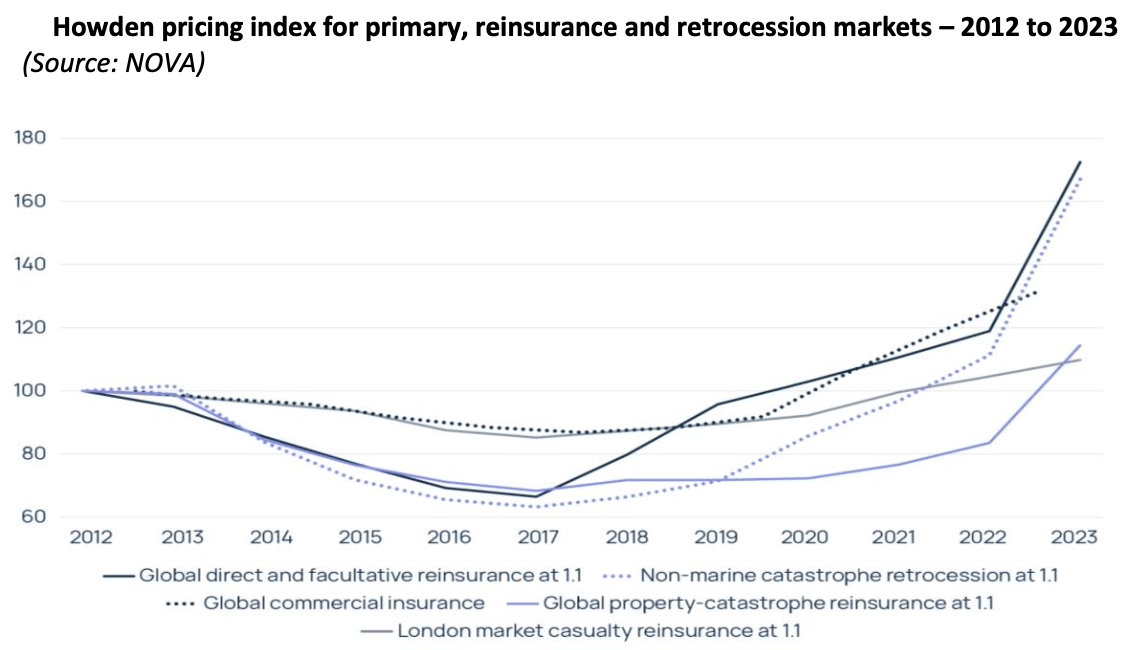

The report also examines the direct and facultative market at the renewals, revealing six consecutive years of significant rate rises, with a marked acceleration of 45% in 2023.

In the casualty space, Howden says that reinsurance supply dynamics remained stable in 2022 and into the Jan 1 2023 renewals, with outcomes similar to those seen last year, with +5% rate rises seen for London market casualty business.