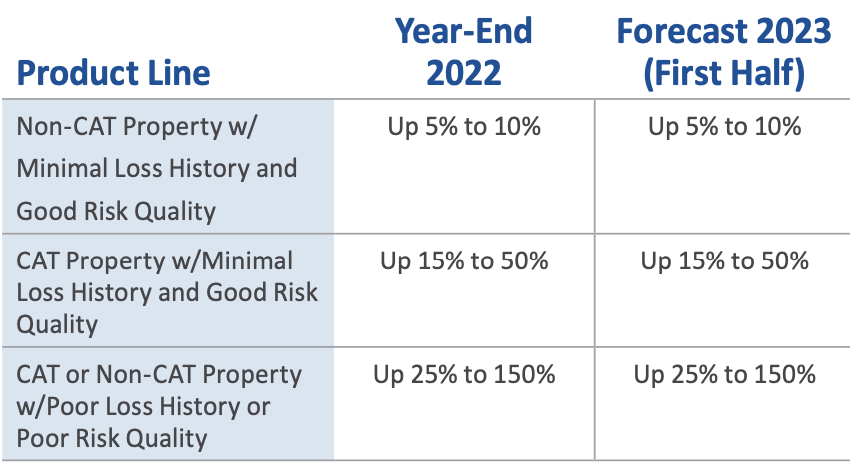

Broker and consulting firm USI Insurance Services has forecast that cat or non-cat property with poor loss history or poor risk quality may see rate increases of up to 150% in the first half of 2023.

![]() Following three years of a firming market with increased deductibles, valuation adjustments, and reductions in capacity, the collective property market was looking forward to some stabilisation in the second half of 2023 or early 2024, explains USI.

Following three years of a firming market with increased deductibles, valuation adjustments, and reductions in capacity, the collective property market was looking forward to some stabilisation in the second half of 2023 or early 2024, explains USI.

However, in the aftermath of Hurricanes Ian and Nicole, a return to a more stable market environment in the near future is unlikely as global insured losses continue to outpace historical averages.

Further, Insurers are grappling with the decreased supply of and increased demand for reinsurance, with global dedicated reinsurance capacity reduced by over $40 billion in the past year alone, says USI.

It writes, “With minimal new meaningful capacity entering the market from either the insurance or reinsurance side, insurers entrenched within strict underwriting guidelines, and continued scrutiny on underwriting data provided, 2023 may prove to be the most difficult property renewal season yet.”

USI suggests that challenges will persist in 2023 for risks with significant exposure to wildfire, named storm, convective storm and flood.

It adds that certain occupancies like food, habitational, wood products, recycling and frame builder’s risk projects will continue to face pressure to improve risk quality while experiencing rate increases, limited capacity and increased deductibles.

USI expects that reinsurance treaty renewals on January 1, 2023, to finalise at rate increases of 20% or more with a limited supply available due to losses, increased exposure basis from raw material costs and supply-chain disruptions, alongside an increased demand from insurers.

Meanwhile, renewals effective in the second half of 2023 may experience limited supply of necessary capacity from their incumbents as portfolio catastrophic event (CAT) aggregates are depleted with little to no opportunity to replace it.

The firm notes, “Insureds will continue to face difficult decisions balancing risk tolerance, third-party insurance requirements and budgetary restrictions.”