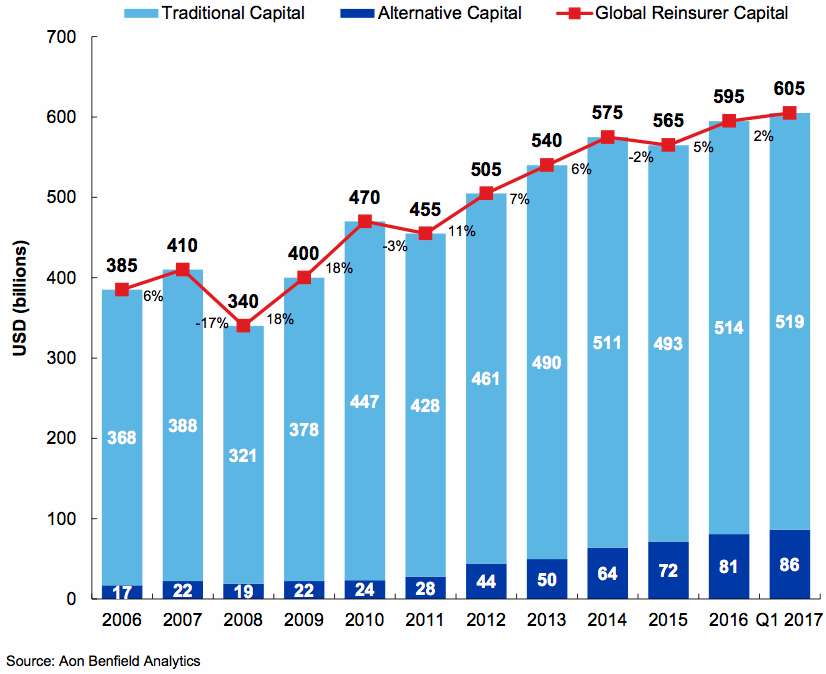

Global, dedicated reinsurance capital increased by 2% to a new high of $605 billion in the first three months of 2017, and with excess capacity remaining a dominant feature of the marketplace, buyers took advantage of favourable conditions at mid-year renewals, according to Aon Benfield.

Aon Benfield, the global reinsurance arm of brokerage Aon, has released its June and July 2017 Reinsurance Market Outlook, which shows that both traditional and alternative reinsurance capital continued to expand in the first-quarter of this year.

When compared with the end of 2016, dedicated reinsurance capital increased by 2% from $595 billion to $605 billion. Traditional reinsurance capital grew by 1% in the period to $519 billion, which Aon Benfield says was driven by retained earnings.

Alternative reinsurance capital growth continued to outpace the traditional side, increasing by 7% in the opening three months of the year to $86 billion, when compared with the end of 2016.

The chart below, provided by Aon Benfield, shows the growth of global, dedicated reinsurance capital since 2006.

The report reveals that the Aon Benfield Aggregate (ABA) reinsurers posted a return on common equity of 8% for the period, a combined ratio of 94.1%, and an ordinary investment yield of 2.7%.

As a result of the benign loss environment, intense competition from both traditional and alternative players, low-interest rates and ample capacity, excess capacity continues to pressure the international reinsurance sector, and “most buyers were able to achieve further cost savings and/or enhanced coverage,” according to Aon Benfield.

The reinsurance broker states that the impact of heightened competition from alternative capital ensured pricing remained under pressure across most classes of business at the recent mid-year property catastrophe renewals.

The mid-year renewal season primarily concern business in the U.S., Australia, New Zealand, Latin America and other smaller markets around the globe, and Australian and New Zealand insurers renewed with “favorable outcomes for insurers overall.”

The well-modelled Florida market experienced an intensification of competition, as a vendor model update resulted in lower expected losses on natural catastrophe risks, while insurance-linked securities (ILS) funds also competed strongly at the mid-year renewals, “offering increased collateralized capacity at decreased pricing margins and expanded coverage relative to prior years.”