According to S&P Global Ratings, the Russia-Ukraine conflict will add uncertainty and exacerbate earnings volatility in global reinsurers’ specialty lines, although their direct asset exposure is minimal.

S&P Global Ratings credit analyst Johannes Bender explained: “For most of the top 21 global reinsurers we rate, asset exposure to Russia and Ukraine is not material, representing less than 2% of total adjusted capital and below 1% of total assets.”

S&P Global Ratings credit analyst Johannes Bender explained: “For most of the top 21 global reinsurers we rate, asset exposure to Russia and Ukraine is not material, representing less than 2% of total adjusted capital and below 1% of total assets.”

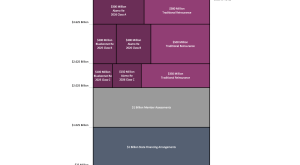

On the liability side however, S&P believes that reinsurers are more exposed to the conflict, particularly in specialty lines, the industry segment that writes more difficult or unusual risks, such as war risk, political violence, and cyber risk, the report says.

“Our scenario analysis indicates that losses from specialty lines are likely to be an earnings event for most reinsurers, but could become a capital event for a few outliers,” Bender said. “We believe global reinsurers will likely assume about one-half of the potential specialty insurance losses.”

S&P’s sector outlook on the global reinsurance industry is negative, reflecting ongoing challenges to meet cost of capital, worsened by first-quarter natural catastrophe losses, the Russia-Ukraine conflict, and rising inflation.

At the same time, S&P expects reinsurance positive pricing momentum to continue in the upcoming renewals in 2022. Furthermore, capitalisation remains a key strength for the sector.

In the rating agency’s view, the top 21 global reinsurers will likely assume about one-half of the potential losses in the insurance sector on aggregate. The losses assumed by reinsurers will vary by line of business because certain lines are more reinsured than others.

For most reinsurers, the Russia-Ukraine conflict losses could be an earnings event. However, it could turn into a capital event for a few outliers given the large natural catastrophe losses already accumulating in the first quarter 2022 even before the Atlantic and Pacific hurricane seasons start.

These negative outliers’ profiles are likely to be more concentrated within the specialty lines with large market shares.

This bumpy start to 2022, as well as rising inflation that will hit both the asset and the liability side, means the industry is likely to find it difficult to meet its cost of capital (COC) once again in 2022.

The year 2021 was the fourth in the past five years (2017-2021) in which the sector did not earn its COC, and as a result, the rating agency maintains its negative outlook on the global reinsurance sector.

This decision reflects on its expectation of credit trends over the next 12 months, including the current distribution of rating outlooks, existing sector-wide risks, and emerging risks.

As of March 31, 2022, 29% of ratings on the top 21 global reinsurers had negative outlooks, 57% outlooks were stable, and 14% were positive or on CreditWatch with positive implications.