A group of re/insurers tracked by Willis Re reported improved combined ratios through the first nine months of the year despite elevated catastrophe losses in the third quarter, while half the cohort achieved double-digit growth in premiums.

A recent report by Willis Re, which explores the 9M 2021 performance of the world’s biggest re/insurers globally who have meaningful commercial lines or reinsurance operations, highlights robust premium growth on the back of pricing and improving economies.

Across the cohort, growth in premiums for both the nine month period and the third quarter was mostly driven by continued favourable pricing for commercial lines business and the improving economic landscape.

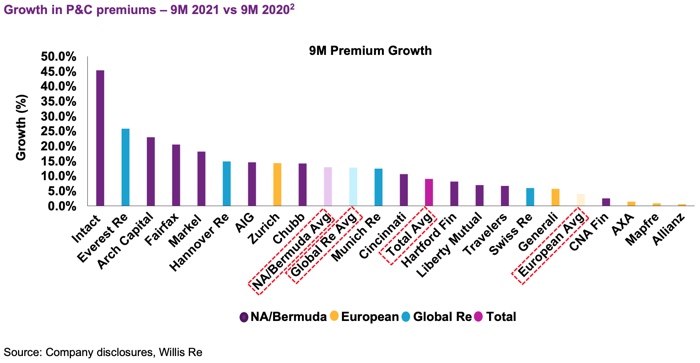

The chart below, provided by Willis Re, shows the cohort’s premium growth over 9M 2021, revealing that half of the companies achieved a double-digit increase.

For both 9M and Q3 2021, Intact tops the list when it comes to premium growth as a result of its acquisition of RSA’s Canadian and UK operations.

Alongside year-on-year premium growth, the group of re/insurers reported an average combined ratio of 95.8% for 9M 2021, compared with 99.3% a year earlier.

“While rates are likely outpacing loss cost trends for most lines of business, with the COVID effects of last year, YOY trends are not good guidance for underlying accident year loss ratio improvement.

“However, it is evident that higher premium growth from the economic rebound and ongoing favourable expense trends continuing post-COVID have helped combined ratios in 2021,” says the reinsurance broker.

After a more benign Q2, re/insurers experienced an elevated catastrophe experience in the third quarter as hurricane Ida battered parts of the U.S. and flooding devastated parts of Europe in July.

While these higher losses were somewhat offset by lower COVID-19 related losses and favourable reserve development, the Q3 2021 combined ratio for the group deteriorated to 99.9%, compared with 99.4% for the same period last year.

“We expect the recent experience and trend to continue to drive a heightened focus on modelling exposure (particularly for secondary perils and climate change), the sufficiency of reinsurance (or retrocession) protection in place, and whether exposures are being adequately reflected in price (both in original and reinsurance terms),” says the broker.